[This article was originally published on GeekWire, June 9, 2011. ]

I’ve met a lot of really bright engineers and entrepreneurs who I think could do great things if they pursued a big, interesting problem in a big, interesting market. But instead they get enamored of scratching their own itch, i.e., solving a problem they themselves have experienced and then didn’t find, didn’t like or didn’t even look for someone else’s solution to the problem.

I’ve met a lot of really bright engineers and entrepreneurs who I think could do great things if they pursued a big, interesting problem in a big, interesting market. But instead they get enamored of scratching their own itch, i.e., solving a problem they themselves have experienced and then didn’t find, didn’t like or didn’t even look for someone else’s solution to the problem.

What’s wrong with that approach?

There was a time when I would have said:  “Nothing, it’s great.” And I still think it can be great. But I no longer think it’s definitely great. Regrettably, too many otherwise really, really smart people believe that doggedly attacking their private obsession with great passion is THE way to do a startup.

“Nothing, it’s great.” And I still think it can be great. But I no longer think it’s definitely great. Regrettably, too many otherwise really, really smart people believe that doggedly attacking their private obsession with great passion is THE way to do a startup.

Sorry. That’s just wrong. And it’s got me rethinking the role and value of entrepreneurial passion.

We’ve all heard the stories of entrepreneurs who experienced a problem and then attacked the problem, fanatically, until they figured out a simple solution. They built a prototype, raised seed capital, worked hard and then sold to Google for a ton of cash.

Some of the stories include apocryphal accounts of entrepreneurs who believed against all odds that their idea was meaningful and would amount to something, even in the face of dozens and dozens of investor rejections, colleague admonitions and the cold shoulder from customers.

See, the myth goes, all you have to do is passionately pursue a solution to a problem you’ve experienced and you’ll be rewarded. Believe in your dream. Prove them all wrong. Never give up. Bullshit! There are two major reasons why passion alone for your idea can be dangerous.

1) Your idea doesn’t know a damn thing about business.

There are countless ideas that I, you, and everyone else, have that just do not warrant spending any more than “hobby time” on. If you want to create a business (which I read somewhere is the point of being an entrepreneur) solving a problem isn’t, well, the problem.

Solving a problem in a way that creates value sufficient to justify someone paying money for the solution (an amount of money sufficient to sustain and grow the business) is the problem.

Investors have a nose for this. And, if your problem doesn’t smell like one that people will (eventually) pay enough money for, then they are unlikely to invest. And if you’re gonna bootstrap (i.e., not take Other Peoples’ Money) then you need to get QUALIFIED external validation of your business because you won’t be getting it from your investors.

Your wife, your best friend, your co-worker, your aunt Judy and your neighbor are not qualified to give you advice on whether your idea might also be a viable business.

If I were going to bootstrap a new business, I’d still look to talk to investors for feedback on my idea as a business. Short of that, find some serial entrepreneurs to talk to, preferably ones who have lots of arrows in their backs.

2) Your passion doesn’t know a damn thing about business.

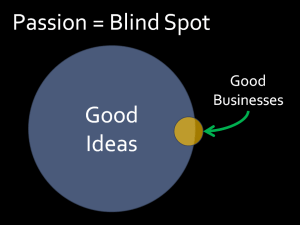

Passion is by definition not rational; and it’s certainly not business savvy. I would go so far as to say that passion (a close cousin of faith and love) is blind. Be careful. I get a little shiver up my spine whenever I hear an entrepreneur justify what they’re working on because it’s a problem they’ve experienced.

It’s as if the mere existence of their passion is what is going to make the difference in their success or, worse, that their passion is what qualifies them to solve the problem in the first place.

The reality is that mere passion about an idea is not a good reason to pursue it; nor is it an indicator that you’re capable or qualified to solve the problem you experience. In fact, the more passionate you are about an idea the more vigilant you should be about getting QUALIFIED third-party validation that your idea could actually be a business.

I don’t mean that you shouldn’t trust yourself. But I do mean that you should not trust an irrational, emotional drive to solve a problem as evidence that the problem is worth trying to build a business around.

Even if there is a business that could be built around solving that problem, that doesn’t mean that you are the one who can solve it. If you get some business validation around the idea and it is in the realm of possibility that you could build that business then your passion may turn out to be an asset.

Now that I’ve railed on passion, I have a confession to make.

I am a dangerously passionate entrepreneur. I also believe that passion is a tremendous asset to entrepreneurs. I would characterize it as necessary, but not sufficient. So what’s passion good for?

Passion can be the spark that gets you going. And it can be the fuel that keeps you going. It will keep you awake late nights. It will inspire confidence as you build a team, raise capital and engage early customers.

There are better things to be passionate about than scratching your own itch. Be passionate about building a great team, passionate about designing a great product, passionate about delighting your customers, passionate about making a difference in people’s lives, passionate about finding and scaling a sustainable business model.

These passions will serve you well whether you’re solving your own problem or someone else’s problem.

But passion just about your personal experience is actually shaky ground.

If you’re so passionate about solving your own problem, then you risk missing some really important things. For example, your market might share your problem too. But they might think about in a very different way.

If your passion about your solution to the problem is incongruous with the way your potential customers think about the problem then you’re in for a tough run. Beyond that, lots of startups end up pivoting their product/market/business pretty substantially away from where they started. This is healthy.

But, if you’re obsessive about solving your problem your way, then you may just miss the real market opportunity. And, if you end up pivoting and land on a product/market that you’re not as passionate about, then you’ll have lost the motivation that got you started in the first place.

Passion may just keep you in the game when nothing else will. When the dark days come (as they usually do) it can be hard to keep going. In the dark of night when you’re running out of money and can’t make payroll, your competitors are beating you badly, you’re being sued by a former employee and 1,000 other things that suck, your passion for the business can keep you from returning that call from the Amazon recruiter.

A closing thought.

If we had to wait around for entrepreneurs, first to suffer from every problem worth fixing, and we had to wait around for the ones who were also passionate about fixing it, and we had to wait around for them to successfully build a viable and sustainable solution, then not very many problems would get fixed. And not very many successful businesses would be built.

and we had to wait around for them to successfully build a viable and sustainable solution, then not very many problems would get fixed. And not very many successful businesses would be built.

If you personally experience a problem in a way that makes you passionate about building a solution then congratulations — you have a reason to think about whether there is possibly a viable business that is worth spending time on. Now, go formulate and test your assumptions about the problem, the solution, the market, the revenue. In short, first strap a spreadsheet to your passion and then see how high you can fly.

grow the pool of startup dev talent in Seattle. I suspect that the lucky folks who participate are going to have crazy-good job opportunities making serious bank — and many of them will find themselves in the right place at the right time and ride a killer startup to a life changing exit (although I don’t think the program guarantees that 😉 Here’s some deets on the program:

grow the pool of startup dev talent in Seattle. I suspect that the lucky folks who participate are going to have crazy-good job opportunities making serious bank — and many of them will find themselves in the right place at the right time and ride a killer startup to a life changing exit (although I don’t think the program guarantees that 😉 Here’s some deets on the program: